A home auction is a public sale where a property goes to the highest bidder, typically sold as-is with strict deposit requirements and no contingencies. Understanding how auction home sales work is the first step to deciding whether this method fits your situation as a homeowner or investor. The process moves fast, demands financial preparation, and offers real transparency that traditional listings rarely match. Auctions follow a defined structure governed by state law, auctioneer licensing requirements, and contract terms that bind both buyer and seller the moment the gavel falls.

How does the home auction process work from start to finish?

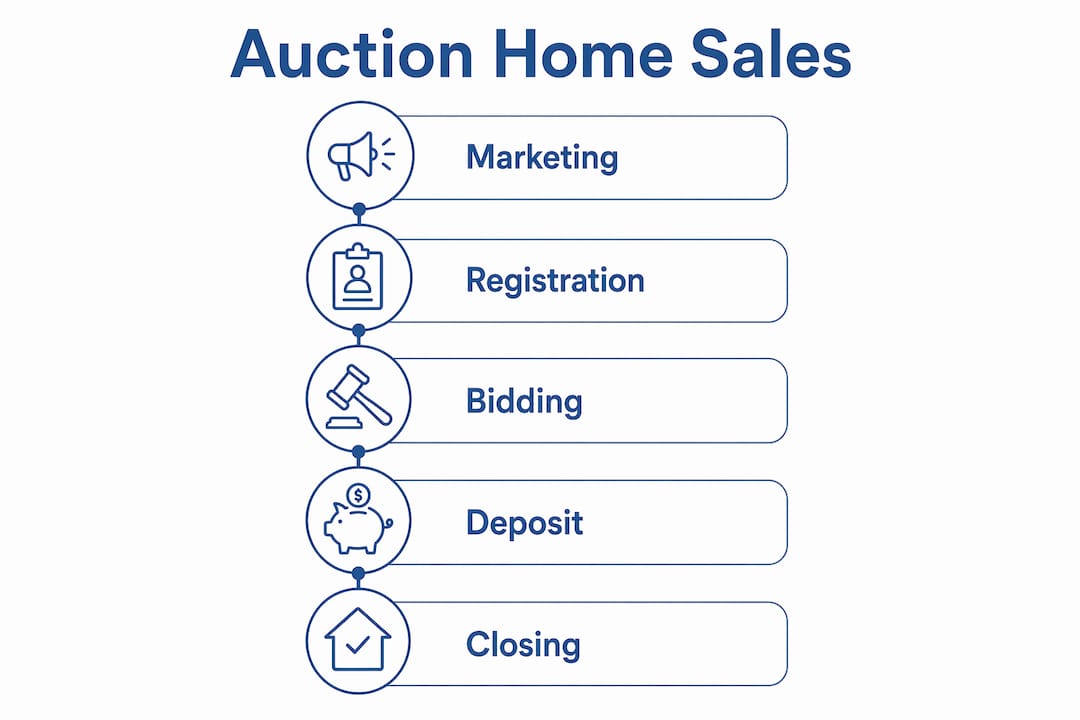

The real estate auction process follows a clear sequence. It begins weeks before auction day and ends at closing, usually faster than a traditional sale.

Step 1: Marketing and inspection period

Professional residential auctions run marketing campaigns 3–6 weeks long, including scheduled public inspection dates. That window gives buyers time to research the property, review disclosures, and arrange financing. Skipping this phase is the most common mistake buyers make.

Step 2: Registration

Bidders must register before auction day. Registration typically requires a government-issued ID and proof of funds or a deposit check. Some online auctions require pre-approval documentation uploaded in advance.

Step 3: Auction day bidding

The auctioneer opens bidding, often at or above a reserve price set by the seller. The reserve price is the minimum the seller will accept. Bidding continues until no higher offer comes in, and the highest bidder wins.

Step 4: Immediate deposit

Winning bidders must pay a deposit on the spot. Earnest money deposits commonly range from 5% to 20% of the purchase price. That deposit is non-refundable in most cases, so walking away after winning costs you real money.

Step 5: Full payment and closing

Full payment is due within 24–72 hours in most auctions. Closing follows shortly after, transferring title to the buyer. The entire process from auction day to closing can take as little as two weeks.

Pro Tip: Attend at least one auction as an observer before you bid. Watch how the auctioneer manages pace, how other bidders behave, and how quickly the deposit process unfolds. That experience is worth more than any guide.

What financial and legal obligations do buyers face at home auctions?

Buying a house at auction carries financial commitments that differ sharply from a traditional purchase. You need to understand every cost before you raise your paddle.

- Buyer's premium: Most auctions charge a buyer's premium on top of the winning bid. Buyer's premiums in residential auctions typically range from 5% to 15% of the purchase price. On a $400,000 winning bid, that adds $20,000 to $60,000 to your total cost.

- As-is condition: Auctions almost always sell properties strictly as-is, with no legal recourse to renegotiate or cancel after the winning bid. Whatever condition the home is in on auction day is the condition you accept.

- Title and lien risks: Liens such as IRS tax debts or HOA fees may survive foreclosure auctions, creating post-sale liabilities the buyer must resolve. That means you could win a property and immediately owe back taxes you did not create.

- Occupancy risks: Some auction properties still have occupants. Evicting a tenant or former owner after purchase adds legal costs and delays that can stretch months.

- No inspection contingencies: You cannot make your bid conditional on a home inspection. Whatever you find after closing is your problem to fix.

Pro Tip: Order a title search before auction day, not after. A qualified real estate attorney can review it and flag any liens or ownership disputes that would survive the sale. That $300–$500 investment can save you tens of thousands.

Buyers who treat auction purchases like traditional home purchases get burned. The protections built into a standard real estate contract, such as inspection periods, financing contingencies, and repair negotiations, do not exist here. You are buying a legal interest in a property, not a move-in-ready home with warranties.

How do auction types and foreclosure processes affect your experience?

Not all auctions follow the same rules. The type of auction and the foreclosure process behind it shape your timeline, your risks, and your opportunities.

Judicial vs. non-judicial foreclosure auctions

Judicial foreclosure auctions can take nearly a year to reach sale, while non-judicial "power of sale" auctions can proceed in a few months. That timeline difference matters because longer processes give buyers more research time. It also affects which liens survive the sale, since judicial foreclosures typically wipe out junior liens while non-judicial processes may not.

State law governs which foreclosure type applies. California, for example, primarily uses non-judicial foreclosure, which moves faster but carries different title risks than a court-supervised process.

Auction format comparison

| Format | Setting | Bidding style | Typical timeline |

|---|---|---|---|

| Live in-person | Courthouse or venue | Open outcry | Same-day result |

| Online auction | Web platform | Timed or live | Days to weeks |

| Sealed bid | Submitted privately | No competing bids visible | Set deadline |

| Hybrid | Online plus live floor | Combined | Varies by auctioneer |

Online auctions have grown significantly and now cover a wide range of property types. They offer convenience but remove the real-time social pressure that sometimes drives prices higher at live events. Sealed bid auctions are less common in residential real estate but appear in government surplus sales and some estate liquidations.

Foreclosure type also affects buyer preparation and financing strategies. A fast non-judicial auction gives you less time to arrange hard money loans or complete due diligence. A judicial process gives you more runway but also more competition from experienced investors who have been tracking the case.

What are the main benefits and drawbacks of home auctions?

Auctions offer real advantages for the right seller or buyer. They also carry risks that make them wrong for others.

Benefits of auction sales:

- Speed is the clearest benefit. A property can go from listed to sold in under six weeks, compared to months on the traditional market.

- Transparent competitive bidding establishes market value in real time without negotiation stages. Every bidder sees the same price at the same moment.

- Sellers control the reserve price, which sets a floor below which they will not sell. That protection prevents a distressed sale at an unfair price.

- Auctions attract motivated, pre-qualified buyers. Tire-kickers do not show up with deposit checks.

Drawbacks to weigh carefully:

- The as-is condition requirement puts all repair risk on the buyer. A roof problem discovered after closing is entirely your cost.

- Strict payment deadlines of 24–72 hours eliminate most buyers who rely on traditional mortgage financing.

- Limited inspection access before bidding means you are often estimating repair costs from a walkthrough, not a professional report.

- Buyer's premiums add a meaningful cost that many first-time auction participants forget to budget.

Auctions suit investors with cash or fast financing, sellers who need certainty and speed, and estate administrators who must liquidate property quickly. They are a poor fit for buyers who need mortgage approval time or sellers who want maximum negotiation flexibility.

What practical tips help homeowners and investors succeed at auctions?

Preparation separates profitable auction buyers from costly ones. Follow these practices before you bid on any property.

- Research title and liens first. Pull a preliminary title report and review it with a real estate attorney. Knowing what survives the auction protects you from unexpected post-sale liabilities.

- Set a firm maximum bid. Calculate your all-in cost: winning bid plus buyer's premium plus estimated repairs plus closing costs. Never exceed that number. Auction rooms create emotional pressure that pushes bidders past rational limits.

- Arrange financing before auction day. Hard money loans can be approved in 24–48 hours and are asset-based rather than credit-based, making them the practical choice for auction purchases. Cash is even better.

- Inspect everything accessible. You may not get a formal inspection, but you can walk the property during the public inspection period. Bring a contractor if possible and document every visible issue.

- Hire a real estate attorney early. Contract terms at auction are non-negotiable, but an attorney can help you understand what you are signing before you sign it.

Pro Tip: Budget a repair contingency of at least 10% of your maximum bid on top of your all-in cost estimate. Auction properties rarely come without surprises, and the ones that do are the exception, not the rule.

Key takeaways

Home auctions sell properties to the highest bidder under strict as-is terms, with deposits due immediately and full payment required within 24–72 hours, making preparation and due diligence the deciding factors between profit and loss.

| Point | Details |

|---|---|

| Deposits are immediate | Winning bidders pay 5%–20% on the spot with no refund if they walk away. |

| Buyer's premium adds real cost | Add 5%–15% to your winning bid to calculate your true purchase price. |

| As-is means no recourse | No inspection contingencies or renegotiation exist after the gavel falls. |

| Foreclosure type changes your risk | Judicial auctions wipe more liens; non-judicial auctions move faster but carry more title risk. |

| Financing must be pre-arranged | Hard money loans or cash are the only realistic options given 24–72 hour payment windows. |

My honest read on home auctions after years in real estate

I have watched a lot of buyers walk into auctions with confidence and walk out with regret. The pattern is almost always the same: they underestimated the total cost, skipped the title research, or let the competitive energy in the room push them past their limit.

Auctions are genuinely good tools. They create price transparency that traditional negotiations rarely achieve. For a seller who needs certainty and speed, an auction removes the drawn-out back-and-forth that can drag a sale out for months. For an investor with cash and experience, auctions offer access to properties at prices that reflect real market demand rather than wishful listing prices.

The problem is that auctions demand a level of preparation most people associate with professional investors, not everyday homeowners. The as-is condition, the immediate deposit, the buyer's premium, the lien risks. These are not fine print. They are the core terms of the deal. Buyers who treat them as secondary concerns pay for that mistake after closing.

My honest advice: if you are a homeowner considering selling through auction, understand that you are trading negotiation flexibility for speed and certainty. That trade is worth it in the right circumstances. If you are a buyer, treat every auction property as a business decision, not an emotional one. Run the numbers, hire the attorney, and set your limit before you walk in the door.

The sellers who benefit most from auctions are those who need to move quickly and have realistic price expectations. The buyers who succeed are those who prepare like professionals, even if they are buying their first investment property.

— Abel

Selling fast without auction complexity? Slocashbuyer can help

Auctions work well for some sellers, but the strict timelines, as-is requirements, and uncertain outcomes are not the right fit for everyone. If you own a home in San Luis Obispo and need a fast, straightforward sale without the pressure of auction day, Slocashbuyer offers a direct path forward.

Slocashbuyer buys homes in any condition for cash, with no repairs required, no agent fees, and no hidden costs. You get a fair cash offer and a closing timeline that works for your schedule. Whether you are facing foreclosure, dealing with an inherited property, or simply ready to move on without the hassle of a traditional listing, get a fast cash offer and see what your home is worth today.

FAQ

What is a buyer's premium at a home auction?

A buyer's premium is an additional fee charged on top of the winning bid, typically ranging from 5% to 15% of the purchase price. It is paid by the buyer and added to the total cost at closing.

Can you use a mortgage to buy a house at auction?

Traditional mortgage financing is rarely possible at auctions because full payment is due within 24–72 hours of winning. Most auction buyers use cash or hard money loans, which can be approved in as little as 24–48 hours.

What happens if you win an auction and cannot pay?

If you cannot complete payment after winning, you forfeit your deposit and may face additional legal liability. Deposits of 5%–20% of the purchase price are typically non-refundable.

Do liens disappear after a foreclosure auction?

Not always. Some liens, including IRS tax debts and HOA fees, can survive a foreclosure auction sale. A title search before bidding is the only reliable way to identify which obligations transfer to the buyer.

How long does the home auction process take from start to closing?

The full process typically takes 5–8 weeks from the start of the marketing period through closing. Marketing campaigns run 3–6 weeks, and closing follows within days to a few weeks after auction day.