A home appraisal is a licensed professional's objective estimate of a property's fair market value, required by most mortgage lenders before they approve a loan. Understanding how home appraisal works gives you real power as a seller. You stop guessing and start negotiating from a position of knowledge. The appraiser's job is to protect the lender's investment by confirming the home's value supports the loan amount. Appraisal fees typically run around $400, paid by the buyer and disclosed on the Loan Estimate after application.

How does the home appraisal process work?

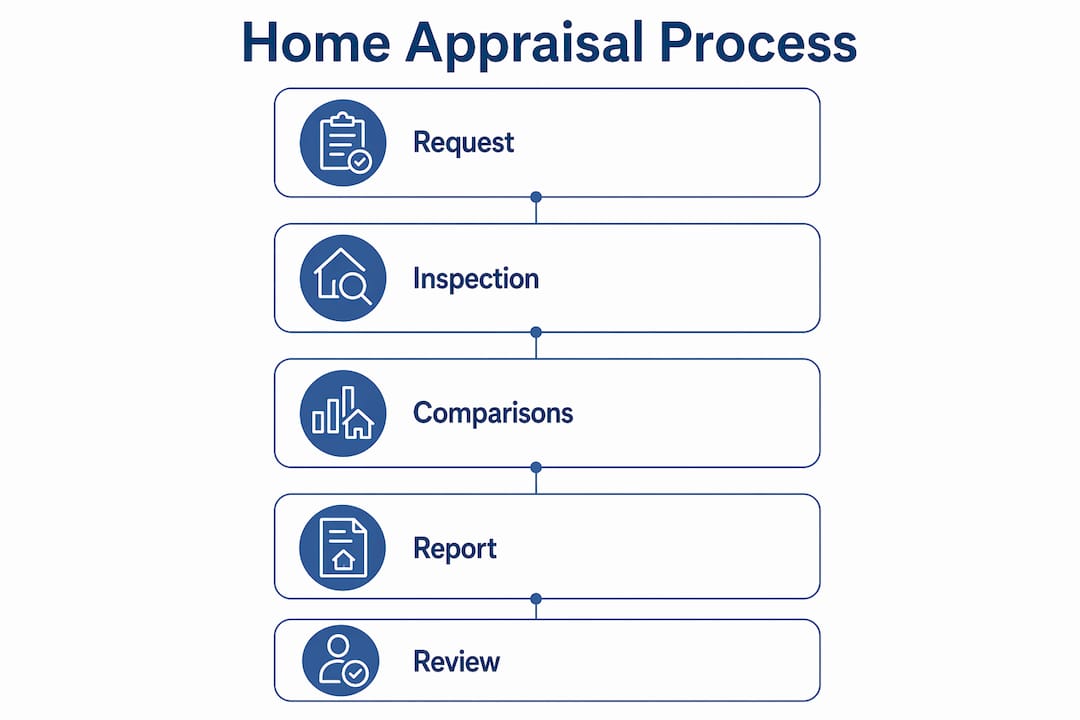

The appraisal process follows a clear sequence. Knowing each step removes the mystery and helps you prepare.

-

The lender places the order. After a buyer submits a loan application, the lender orders the appraisal, often through an appraisal management company. This keeps the appraiser independent from both buyer and seller.

-

The appraiser schedules a visit. You will receive a request to access the property. The visit usually lasts 30 minutes to a few hours depending on home size and condition.

-

The on-site inspection happens. The appraiser verifies home size and condition, checks exterior and interior features, and compares findings against public records. They note upgrades, square footage, lot size, and the condition of major systems visible to the eye.

-

Comparable sales analysis begins. Appraisers pull recent sales of similar homes, typically within a one-mile radius and sold within the past 3–6 months. They adjust values up or down based on differences like garage size, basement finish, or kitchen upgrades.

-

Market conditions get factored in. A rising or falling local market affects the final number. An appraiser in a hot seller's market may weigh recent price trends more heavily.

-

The report gets written. The appraisal report includes estimated market value, photographs, a property description, comparable sales data, and valuation adjustments. The lender receives it first; you can request a copy.

-

Delivery and review. The full process, from order to report delivery, typically takes 1–3 weeks. The on-site visit is the fastest part. Research and report writing take the most time.

Pro Tip: Ask your real estate agent to pull recent comparable sales in your neighborhood before the appraisal. If you spot a strong comp the appraiser might miss, you can mention it during the visit.

What should you expect during the appraisal visit?

The on-site inspection is shorter than most sellers expect. An appraiser is not there to tear apart your home. They are there to observe, measure, and document.

Here is what the appraiser focuses on during the visit:

- Square footage and layout. They measure the home and compare it against public records. Discrepancies get noted.

- Condition of major systems. Roof, HVAC, plumbing, and electrical are observed visually. The appraiser notes obvious issues but does not test systems.

- Upgrades and finishes. A renovated kitchen, new flooring, or a recently replaced roof all factor into value adjustments.

- Exterior condition. Curb appeal, siding, windows, and the driveway all get evaluated.

- Neighborhood context. Proximity to schools, commercial areas, and comparable properties shapes the final opinion of value.

A critical distinction separates appraisals from inspections. Inspections assess how the home functions; appraisals assess what it is worth. An inspector tests the furnace and checks for leaks. An appraiser notes the furnace's age and condition visually. Both serve different purposes, and most lenders require both.

A common misconception is that a good appraisal means the home's systems are fully functional. Appraisers identify major hazards but do not evaluate the operational condition of all home systems. A clean appraisal is not a clean bill of health for the plumbing.

Pro Tip: Tidy up before the visit, but do not obsess over cosmetics. Appraisers are trained to look past clutter. A freshly painted wall will not add $10,000 to your value. A documented roof replacement will.

What happens when the appraisal value misses the contract price?

A low appraisal is one of the most stressful moments in a home sale. When the appraised value comes in below the agreed purchase price, the lender will not approve the full loan amount. That gap has to be resolved before the sale can close.

You have several paths forward:

- Renegotiate the price. The seller and buyer can agree to lower the contract price to match the appraised value. This is the most common resolution.

- The buyer covers the difference. If the buyer has cash reserves, they can pay the gap out of pocket. This keeps the sale price intact but requires the buyer to bring more money to closing.

- Request a Reconsideration of Value. Either party can formally challenge the appraisal by submitting additional comparable sales the appraiser may have missed. This process can delay closing by 1–2 weeks and does not guarantee a different outcome.

- Walk away. If no resolution is reached, the buyer may exercise an appraisal contingency and exit the contract without penalty.

As a seller, a low appraisal does not automatically mean your home is overpriced. Local market data may not yet reflect recent price movement. Lenders use the appraisal to protect their investment, not to set a ceiling on what your home is worth to a motivated buyer. Stay calm, review the comparable sales used, and work with your agent to identify any errors or missing data before accepting a lower price.

How to prepare for a home appraisal as a seller

Preparation directly influences how accurately your home gets valued. Appraisers work from what they can see and document. Your job is to make that as easy as possible.

- Document every upgrade. Compile receipts, permits, and contractor invoices for renovations. A new HVAC system, roof replacement, or kitchen remodel adds real value, but only if the appraiser knows about it. Providing evidence of improvements helps appraisers account for value beyond surface observations.

- List system ages and replacements. Write down when the roof, water heater, HVAC, and major appliances were last replaced. Hand this list to the appraiser at the start of the visit.

- Clear access to all areas. The appraiser needs to see the attic, basement, garage, and all rooms. Locked doors or blocked access create gaps in the report.

- Fix obvious deferred maintenance. A broken handrail, cracked window, or peeling exterior paint signals neglect. These are inexpensive fixes that can prevent negative notes in the report.

- Know your comps. Research recent sales of similar homes in your neighborhood. If you find a strong sale the appraiser might overlook, you can mention it respectfully during the visit.

Pro Tip: Prepare a one-page property summary before the appraisal. Include square footage, year built, recent upgrades with dates, and any unique features like a permitted ADU or solar panels. Hand it to the appraiser when they arrive. It takes ten minutes to create and can meaningfully improve the accuracy of your valuation.

The biggest mistake sellers make is treating the appraisal as something that just happens to them. You have more influence over the outcome than you think, as long as you show up prepared.

Key Takeaways

A home appraisal is a licensed professional's unbiased estimate of market value that protects lenders, informs buyers, and gives sellers a clear benchmark for negotiation.

| Point | Details |

|---|---|

| Appraisal protects the lender | Lenders require appraisals to confirm the home's value supports the loan amount before approval. |

| Process takes 1–3 weeks | The on-site visit is quick; comparable research and report writing take the most time. |

| Appraisal differs from inspection | Appraisers assess market value; inspectors assess how home systems function. |

| Low appraisal triggers options | Sellers can renegotiate price, request a Reconsideration of Value, or let the buyer cover the gap. |

| Preparation improves accuracy | Documenting upgrades and system ages gives appraisers the data they need to value your home fairly. |

What I have learned from watching sellers handle appraisals

Most sellers I have worked with treat the appraisal as a black box. They hand over the keys, wait, and hope for the best. That approach costs them money.

The sellers who come out ahead treat the appraisal like a presentation. They show up with documentation, they know their comparable sales, and they communicate clearly with the appraiser. They do not argue or pressure. They inform. There is a real difference between those two things.

The confusion between appraisal and inspection trips up sellers constantly. I have seen homeowners panic over a low appraisal when the actual issue was a disputed comparable sale, not a problem with the home. And I have seen sellers assume a clean appraisal meant the home was in perfect working order, only to face repair demands after the inspection. These are two separate processes. Keeping them separate in your mind saves you from a lot of unnecessary stress.

The other thing I will say plainly: an appraisal is not your enemy. It is an objective checkpoint. When the number comes in where you expected, it validates your price. When it does not, it gives you information you can act on. Either way, you are better off knowing.

If you are selling in a market with limited comparable sales, like many parts of San Luis Obispo County, preparation matters even more. Appraisers working with thin data rely heavily on what you give them. A well-documented upgrade list can be the difference between a fair valuation and one that leaves money on the table.

— Abel

Selling your home without the appraisal wait

If the appraisal process feels like one more hurdle you do not want to clear, Slocashbuyer offers a different path. We buy homes in any condition for cash in San Luis Obispo, CA, with no repairs required, no agent fees, and no waiting on lender timelines. You get a fair cash offer based on your home's real value, and we handle the rest. Whether you are facing foreclosure, dealing with a property that needs significant work, or simply want to move on quickly, we can help you sell fast without the stress of a traditional sale. Reach out to Slocashbuyer today and get your offer.

FAQ

What is the home appraisal meaning in a real estate sale?

A home appraisal is a licensed appraiser's unbiased estimate of a property's fair market value, required by lenders to confirm the home's price supports the loan amount before approval.

How long does the home appraisal process take?

The full process typically takes 1–3 weeks from order to report delivery, with the on-site visit being the fastest part and comparable research taking the most time.

How do appraisers determine value?

Appraisers compare the home to recent sales of similar properties within roughly a one-mile radius, then adjust values up or down based on differences in size, condition, and features.

What happens if the appraisal comes in low?

A low appraisal means the lender will not approve the full loan amount. The seller and buyer must then renegotiate the price, have the buyer cover the gap in cash, or file a Reconsideration of Value request.

Does a home appraisal replace a home inspection?

No. An appraisal estimates market value while an inspection evaluates how home systems function. Both are typically required in a financed sale, and neither substitutes for the other.